{kind=link}

However during the last 4 years, the COLA has totally protected retirees.

The inflation information for August offers us a fairly good thought in regards to the possible magnitude of Social Safety’s cost-of-living adjustment (COLA) for 2025. This computerized indexing of advantages to maintain up with rising costs – all the time a beautiful function of our Social Safety program – has been significantly helpful in gentle of the current bout of inflation.

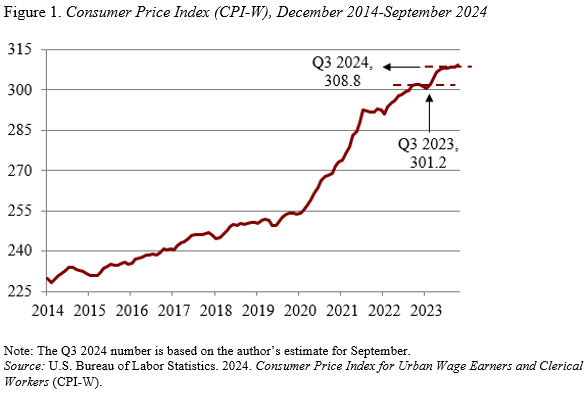

For the reason that COLA first impacts advantages paid after January 1, Social Safety must have figures obtainable earlier than the tip of 2024. In consequence, the adjustment for 2025 will likely be based mostly on the rise within the CPI-W for the third quarter of 2024 over the third quarter of 2023. We all know the 2023 quantity (see Determine 1), however we’d like information for July, August, and September to calculate the third quarter common for 2024. For 2024, we now have the numbers for July and August. Assuming that the September improve is just like that in July and August, the common for the third quarter of 2024 will likely be 308.8, which represents a 2.5-percent improve over the third quarter of 2023. A COLA of two.5 % may be very near the two.6-percent projection within the 2024 Social Safety Trustees Report.

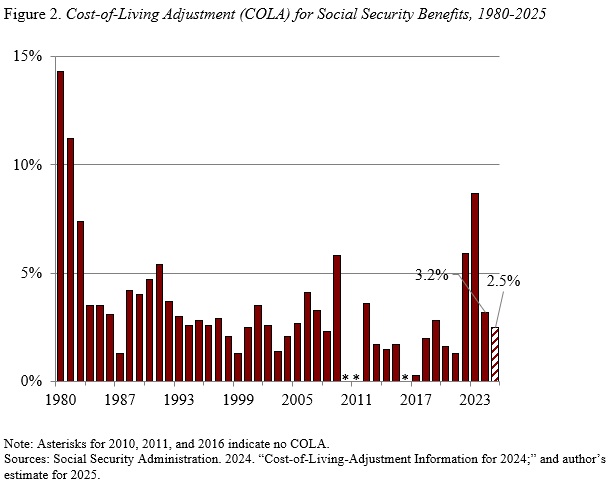

Some bemoan that this yr’s COLA is smaller than these prior to now few years (see Determine 2). However the adjustment is designed to compensate for rising costs, in order inflation drops, the magnitude of the required adjustment additionally falls.

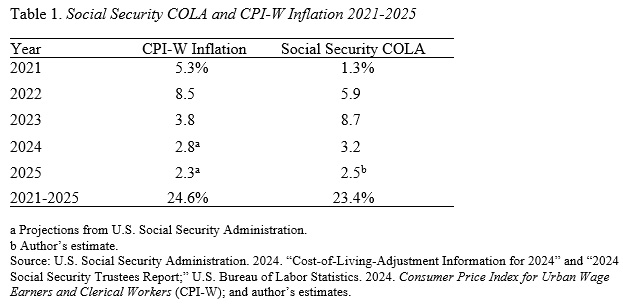

When larger will increase had been required, Social Safety did its job. By design, the timing was not good – the COLA lagged when inflation took off, however then greater than compensated as inflation slowed (see Desk 1). The necessary level, nevertheless, is that over your complete interval, the Social Safety COLA has totally protected retirees from the rise within the CPI-W.

Social Safety’s COLA is likely one of the most dear facets of this system’s design. It has all the time supplied invaluable safety. Even an inflation fee as little as 2 % cuts the buying energy of a $1,000 profit to $600 over a 25-year retirement. The COLA prevents that erosion. However the lack of drama implies that the COLA goes unappreciated. The one good factor that could be mentioned in regards to the present inflation spike – which is dangerous for all facets of our lives – is that it has highlighted the worth of getting retirement advantages that sustain with costs.