{kind=link}

That mentioned, the taxation of Social Safety advantages might be higher designed.

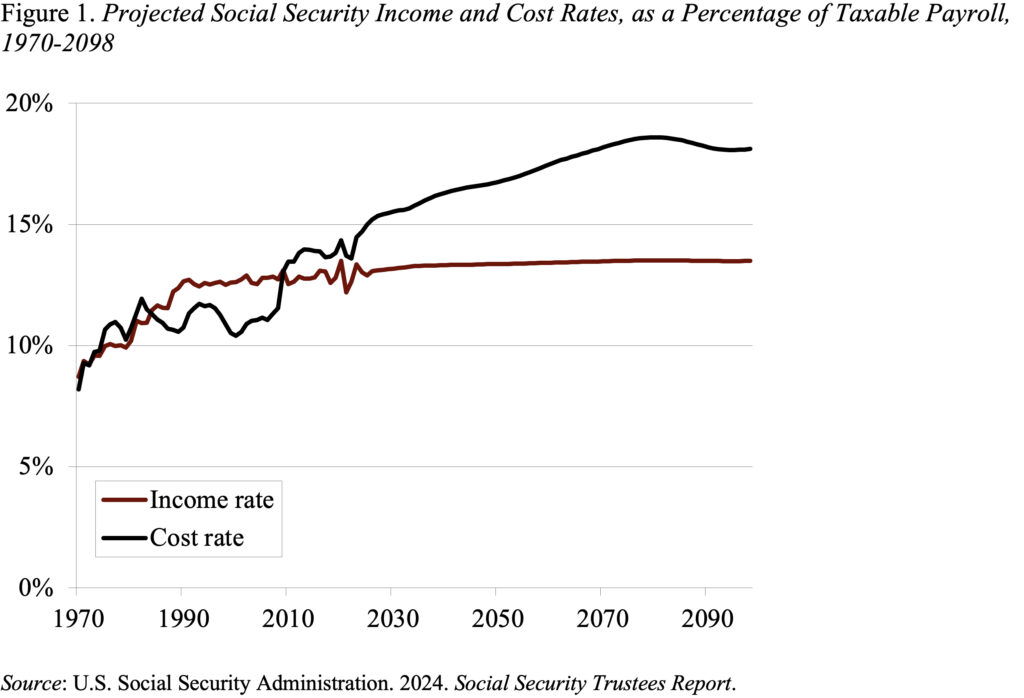

Social Safety, the spine of our retirement system, is going through a financing downside. Prices have been rising and the tax price has been mounted, creating a niche between cash coming in and advantages going out (see Determine 1). Within the quick time period, the federal government is utilizing the belongings within the belief fund – amassed within the wake of the 1983 amendments – to bridge the hole. These belief fund belongings will likely be depleted within the first half of the 2030s, and, if Congress fails to behave, advantages will likely be lower by about 20 %.

To keep up the present degree of advantages – a dedication contained in the Republican get together platform and supported by Democrats – the system wants extra money. So, it’s actually annoying to listen to former President Trump suggest to chop the cash going into this system by eliminating the taxation of Social Safety advantages.

The taxation of advantages, additionally launched in 1983, not solely produces revenues to cowl outlays but additionally helps make the system extra progressive. The profit construction already replaces a a lot bigger share of pre-retirement earnings for the low paid than the excessive paid. The taxation of advantages underneath the federal earnings tax, which imposes greater charges on these with greater incomes, reinforces this aim.

That mentioned, the taxation of Social Safety advantages might be higher designed when it comes to the character of the edge and the share included in earnings.

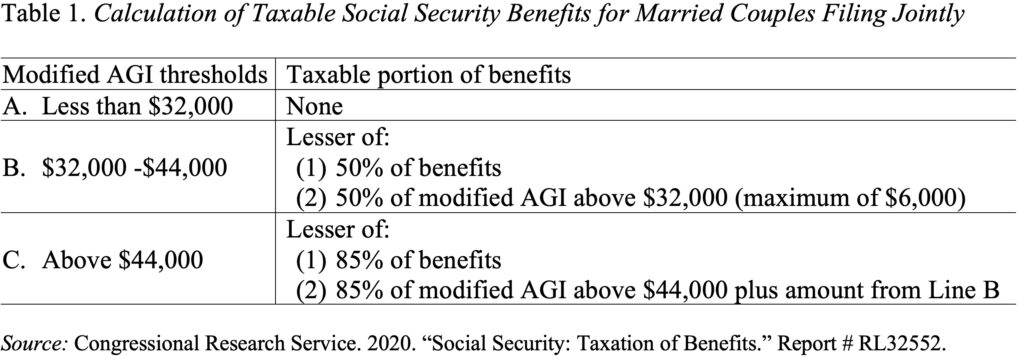

Underneath present regulation, married {couples} with lower than $32,000 of modified adjusted gross earnings (AGI) should not have to pay taxes on their advantages. (“Modified AGI” is AGI as reported on tax varieties plus nontaxable curiosity earnings, curiosity from international sources, and one-half of Social Safety advantages.) Above this threshold, recipients should pay taxes on as much as both 50 % or 85 % of their advantages (see Desk 1).

In contrast to the remainder of the federal earnings tax, the thresholds for calculating Social Safety taxes are not listed for inflation. In consequence, over time inflation forces many who at the moment don’t pay taxes on their advantages to incorporate 50 % of their Social Safety of their tax calculations and plenty of others who solely embody 50 % to pay taxes on as much as 85 %. If policymakers desire a threshold, they need to choose a degree under which individuals should not have to incorporate Social Safety advantages of their earnings after which index that degree for inflation. My view is that nearly every little thing within the coverage world ought to be listed for inflation.

Second, the benchmark for the present method to taxing Social Safety actually doesn’t make sense at present. Whereas outlined profit plans provided an inexpensive benchmark within the Nineteen Eighties, at present most personal sector staff are lined by 401(okay)s. Since 2006, when Roth 401(okay)s grew to become out there, taxes might be levied in two methods. Within the conventional 401(okay), the worker places in pre-tax {dollars} and is taxed when the cash is withdrawn in retirement. Within the Roth 401(okay), the worker places in after-tax {dollars} and pays no tax in retirement. Social Safety contributions might be regarded as one-half conventional and one-half Roth. From this attitude, taxing Social Safety like personal plans would recommend that the half of Social Safety advantages financed by the employer’s pre-tax contribution ought to be taxable in retirement and the Roth-like different half, the place taxes have already been paid, ought to be excluded. In different phrases, at present 50 % – not 85 % – of Social Safety advantages may be seen as the suitable share of advantages to incorporate in adjusted gross earnings.

In brief, a considerate reconsideration of the taxation of Social Safety advantages might be included in any course of to resolve Social Safety’s 75-year financing shortfall. However popping out with a one-off proposal to eradicate all taxation of Social Safety advantages is supremely unhelpful.