{kind=link}

I suspected most monetary property have been in 401(ok) plans and most 401(ok) holdings have been directed by target-date funds, however the knowledge instructed a considerably completely different story.

When making an attempt to determine folks’s style for danger by trying on the share of equities of their monetary portfolio, I used to be questioning in a world of 401(ok)s concerning the extent to which this share would all be decided by the sample of goal date funds. Candidly, my prior was that, for all besides the very wealthy, most family monetary property have been in 401(ok)s and that the majority 401(ok) property have been in goal date funds. It’s all the time helpful, nevertheless, to have a look at slightly knowledge. It seems that my state of affairs shouldn’t be fairly the place we are actually, however may describe the place we’re headed.

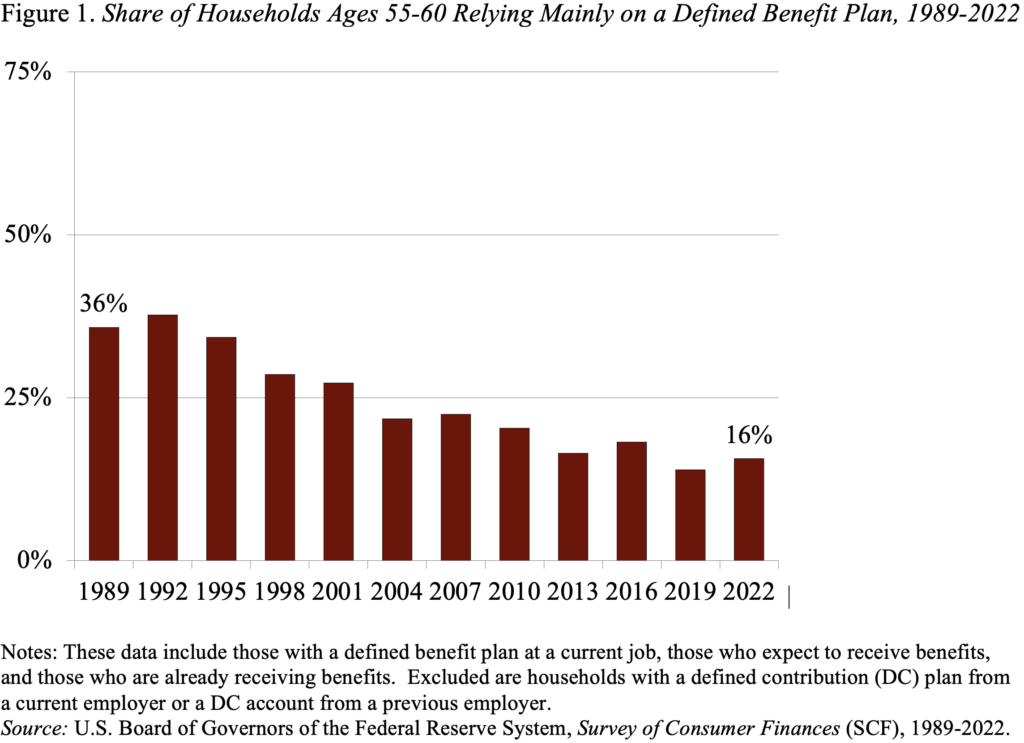

The notion was not a loopy one in that the 2020s signify the primary time that employees might have spent a complete profession coated by a 401(ok) plan. Certainly, solely about 16 % of households approaching retirement in 2022 are relying primarily on an outlined profit plan (see Determine 1). That evolution suggests that the majority retirement saving could now be in 401(ok)s or Particular person Retirement Accounts (IRAs).

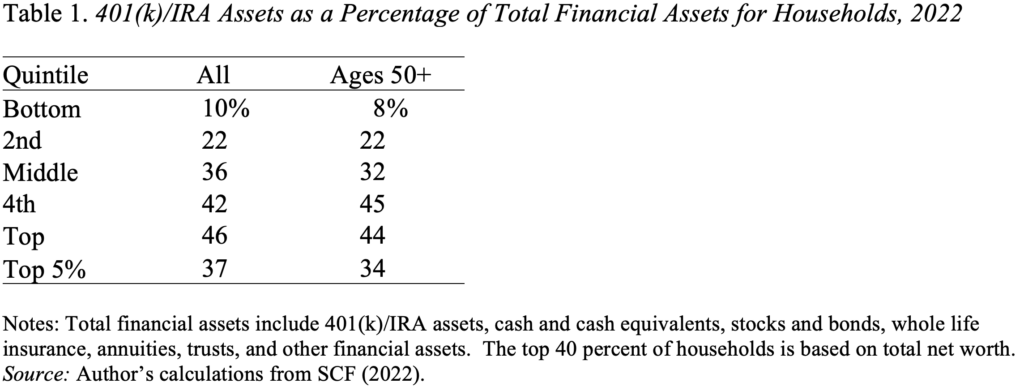

So, the query is what share of economic property are 401(ok)/IRA balances? These percentages for 2022 by web price quintile present that for the highest two quintiles – the highest 40 %, who maintain a lot of the 401(ok) property – retirement property account for about 45 % of complete monetary property (see Desk 1). The richest 5 % scale back the share for the highest quintile as a complete as a result of they maintain a lot in non-retirement property. However, the chances are considerably lower than I had hypothesized.

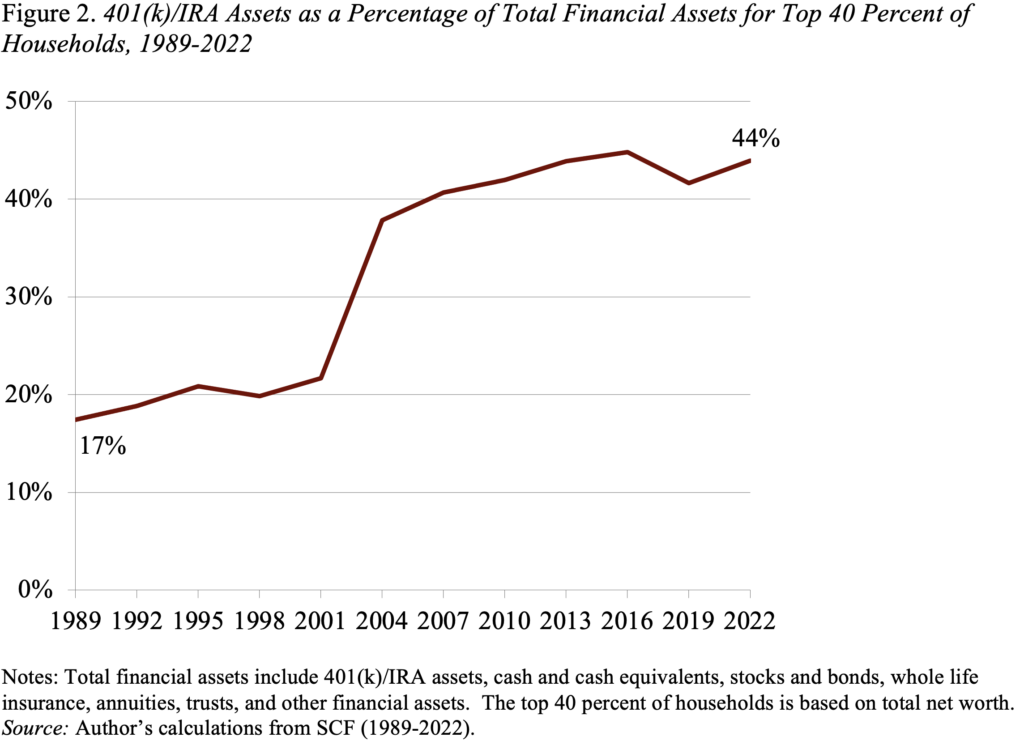

If the state of affairs was not precisely what I assumed, are we not less than trending in that path? Certainly, the share has elevated sharply over time, albeit it’s not clear the place it’s going from right here (see Determine 2).

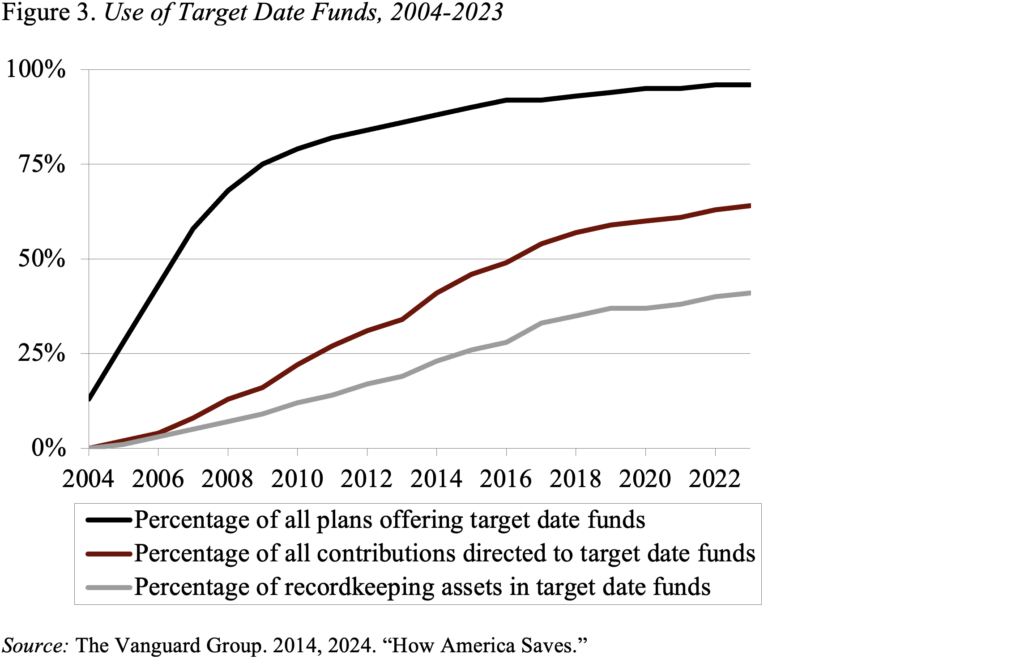

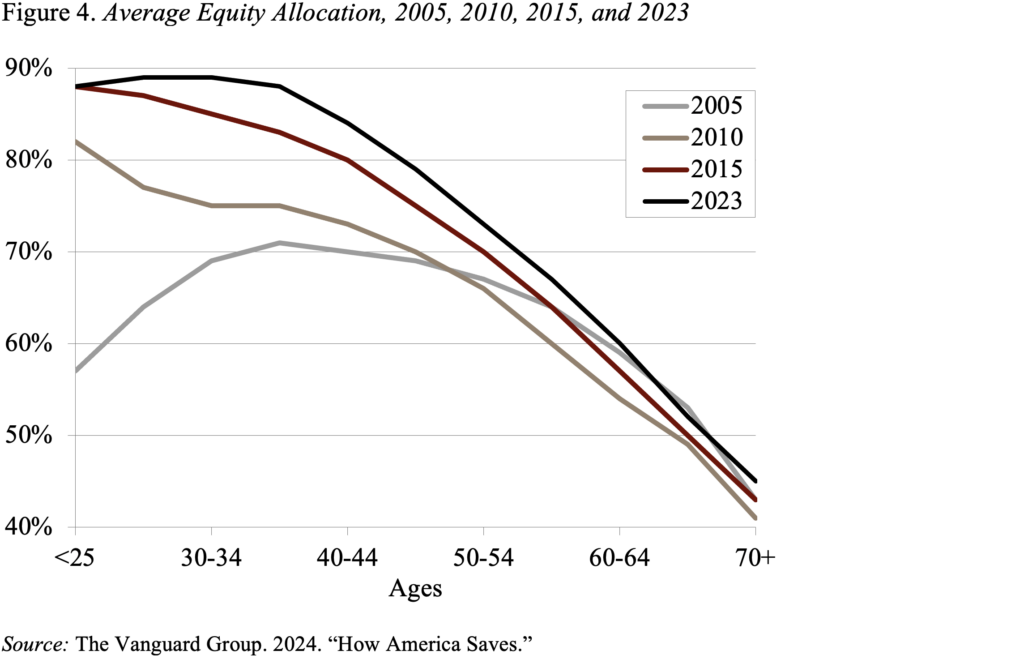

It looks like I used to be additionally slightly forward when it comes to the position of goal date funds (TDFs) – funds that routinely scale back fairness holdings as members age – inside 401(ok)s. It’s not stunning on condition that the massive change got here when the Pension Safety Act of 2006 allowed plan sponsors to routinely enroll workers utilizing TDFs because the default funding. Since then, the share of plans providing, the share of contributions directed towards, and the share of property in TDFs have all been growing quickly (see Determine 3).

Funding in TDFs has modified the profile of asset allocation and elevated holdings in equities (see Determine 4). In 2005, the allocation of equities was hump-shaped; youthful members have been extra conservative, middle-age members held essentially the most equites and older members sharply lowered their holdings. In 2023, the fairness allocation of members sloped downward by age, beginning at 88 % for younger employees, declining to 73 % for these ages 50-54 after which to 45 % for these 70+. Not solely is the sample very completely different, however the share of 401(ok) property in equities has additionally elevated markedly.

So, the story wasn’t as clear as I had thought. For these within the high 40 % of the wealth distribution, retirement property are solely about 45 % of complete property and the share appears secure. Inside 401(ok) plans the significance of goal date funds has been growing over time and is prone to be much more necessary sooner or later. Alternatively, folks have a tendency to maneuver their property out of 401(ok) plans into IRAs and will change their allocations. So, I assume that folks train extra discretion over their fairness holdings than I assumed.