{kind=link}

The minority of Individuals who’ve a monetary adviser say they really feel fairly good about the place they’re. It’s everybody else who is essentially dissatisfied with their funds.

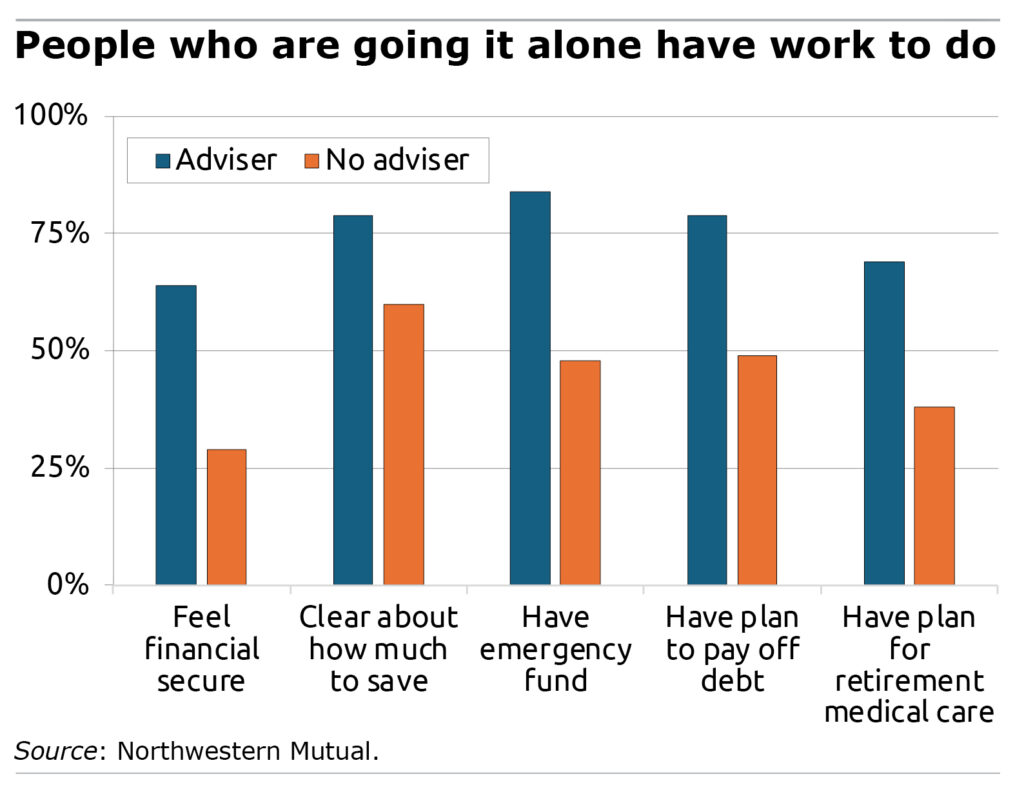

Among the many staff and retirees who seek the advice of a monetary adviser, two out of three describe themselves as financially safe, and the others are presumably engaged on it. Solely one among three individuals who don’t use an adviser are feeling safe, in accordance with Northwestern Mutual’s January survey of greater than 4,500 adults over age 18.

About 80 % of these with an adviser even have a plan for a way they are going to repay debt, whether or not members of Gen Y and Gen Z with pupil loans or child boomers with a mortgage. Solely half with out an adviser do.

The purpose in making these contrasts is to not advocate for hiring an adviser however to focus on the truth that too many Individuals are flailing and are unclear about what they should do to organize for retirement.

Now that private-sector pensions have largely fallen by the wayside, saving is vital. Retirees use it to complement their Social Safety, which replaces about 40 % of a mean retiring 65-year-old’s wages right now. However 4 out of each ten U.S. staff will not be on observe with their financial savings to make sure they are going to be capable to preserve their present life after they retire.

And the variety of individuals in bother can be rather a lot increased if the housing market had not been on an upward trajectory for greater than a decade. Dwelling fairness, like a 401(ok), counts as a type of retirement wealth. However in observe, it’s not a lot use to retirees as a result of they don’t normally faucet it to help their residing requirements.

A big majority of the individuals in Northwestern’s survey who make use of advisers stated they’re clear concerning the tradeoff between spending now and saving for later. Working with an adviser offers the “readability that folks don’t have on their very own,” argues Hanna Grichanik, a monetary adviser with Northwestern Mutual.

One other instance is an emergency fund. Grichanik says it’s simply as vital for a retiree to have one as a employee. However their causes differ considerably. Employees who’ve an emergency fund for sudden bills don’t need to deplete the cash they’re saving for a retirement nonetheless a few years away. Retirees additionally want money for the sudden. If they’ve an emergency fund, they will higher time their common withdrawals from retirement financial savings. They “don’t need to take cash out [of savings] when the market is down. It’s the identical motive individuals don’t promote their dwelling at a depressed value,” she stated.

Whether or not somebody chooses to rent an adviser or not, planning is vital. “Intention results in higher outcomes,” Grichanik stated. The problems Northwestern asks about in its survey – saving for retirement, an emergency fund, a plan to repay debt – are a information to what must be finished to really feel financially safe. It takes work.

Squared Away author Kim Blanton invitations you to comply with us @SquaredAwayBC on X, previously referred to as Twitter. To remain present on our weblog, be a part of our free electronic mail listing. You’ll obtain only one electronic mail every week – with hyperlinks to the 2 new posts for that week – while you enroll right here. This weblog is supported by the Middle for Retirement Analysis at Boston School.